Investing in European equities

Finding the opportunities among oil and luxury goods stocks

European stocks have been dominated by large unfashionable companies or businesses that have a big presence in the luxury goods market but come with hefty valuations.

But as lockdowns ease and vaccinations get into full swing, European shares hold promise for investors, if they know what to look for.

As growth is slowing in emerging markets, Europe is offering opportunities, but investors have to search further for unappreciated, smaller businesses rather than rely on the big, well-known ones for returns.

This article, which qualifies for 30 minutes' CPD, aims to set out some of the issues related to investing in Europe.

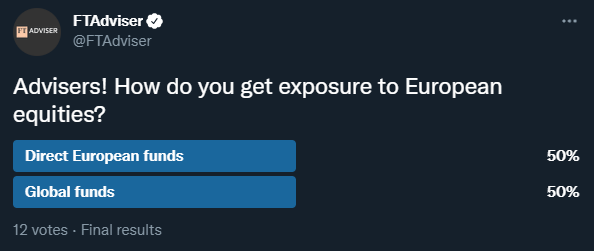

By a small majority, advisers are planning to add to their European equity exposure in the year ahead, according to the latest FTAdviser poll.

The poll showed that, by a majority of 58 per cent to 41 per cent, advisers intend to increase their exposure to European equities in the year ahead.

The Euro Stoxx Index of European shares is down this year to date, from a starting point of 3,793 points, to the current level of 3,245.

Over the past five years the index has fallen from 3,637 to the current level.

And flows data has been similarly negative, with investors withdrawing £451m from funds within the sector in May, compared with a net inflow of £253m into the IA UK All Companies sector in the same time period.

Tommy Faber, equity fund manager at Waverton Investment Management, says European equities have generally been out of favour with global investors in recent years, as the region is viewed as being full of companies that lack technological expertise and a desire to maximise shareholder value.

But he says while the region as a whole may have such issues, there are always individual companies within Europe that are a good investment.

Pexels/Tuur Tisseghem

Pexels/Tuur Tisseghem

Michaela Handrek-Rehle/Bloomberg

Michaela Handrek-Rehle/Bloomberg

Hollie Adams/Bloomberg

Hollie Adams/Bloomberg

Should your client be invested in European equities?

The investment case for European equities has been dogged by swirls of negative sentiment around the long-term outlook for the economy.

The composition of numerous Eurozone indices is also an issue for many, with the market stuffed with the kind of commodity and 'old economy' shares that have rapidly fallen out of favour with many clients, who are keen to embrace technology and 'new economy' stocks.

The economic issue, according to Guillaume Paillat, multi-asset investor at Aviva Investors, is that the Eurozone has been mired in what economists call “secular stagnation” for much of the past decade.

This phenomenon is characterised by low levels of economic growth and low inflation, caused by the 'three Ds': high levels of debt; ageing populations causing poor demographics; and technological disruption leaving many companies in the economic bloc with impaired business models.

Simon Edelsten, who runs the £500m Mid Wynd investment trust, says in addition to the long-term economic issues impacting the bloc, the Eurozone is also vulnerable to pandemic-specific issues, as the growth slowdown in emerging markets hurts the export-based economies of northern Europe, while the tourism-focused economies of southern Europe suffered as a result of travel restrictions.

Hugh Cuthbert, European equity fund manager at SVM, says: “The economic issues in Europe have not gone away, but what has potentially happened is that the pandemic has brought issues like high debt levels to other parts of the world as well, so Europe may no longer be the outlier."

He adds: “The slowdown in emerging markets probably does hurt a lot of companies, but I think the European equity market’s USP is that it has a lot of high-quality luxury goods companies, or companies with very strong consumer brands, and I think those will be fine.

“Growth is slowing in emerging markets, but it is not an actual recession, and in those circumstances, the higher quality European consumer goods companies should do well. The issue really is that luxury goods companies trade on expensive valuations, so it may be better to look elsewhere.”

Will James, who runs the European equity income fund at Premier Miton, says: “It is 10 years since Europe was rocked by the sovereign debt crisis, which in one fell swoop took any real, relative attraction that Europe may have had in the recovery phase post the global financial crisis.

“In spite of [Italian Prime Minister] Mario Draghi’s best efforts to do ‘whatever it takes’ to save the Euro, an already sceptical international investor community had their biases reinforced that Europe was a structurally challenged entity where politics, populism and a paucity of growth would prevail. As a result, any allocation to Europe was grudging at best.”

Hywel Franklin, head of European equities at Mirabaud Asset Management, says that with the issues in the European economy so well-known, “one has to just focus on valuation. Everything has a price. I think a big part of it is people focus relentlessly on the biggest companies, where there is plenty known about their prospects".

He adds: “But there are a lot of smaller companies that are under the radar for most investors. The larger companies are often in the less attractive sectors, such as banking or oil, whereas the smaller part of the market has lots of world-class companies that operate in specific niches.”

SVM's Cuthbert says banks may deliver strong returns if interest rates rise.

Aviva's Paillat says the longer-term outlook for European equities is more positive because while it remains a market that does best when the wider economy is growing, what has changed is the quality of the cyclical companies.

He says the market had been dominated by cyclical companies in areas such as oil and mining, which he defines as “low quality”, while the market is changing to encompass more of the higher quality cyclical companies, such as luxury businesses, which are world class at what they do, and so have market positions that are more readily defendable than those of commodity companies or banks.

Rob Harley, European sustainable equity fund manager at Stewart Investors, says that as investors increasingly focus on sustainability and the new economy, many of the leading companies in the renewable energy and disruptive healthcare space are listed in Europe.

Harley acknowledges that such companies tend to trade at expensive valuations, but says that such is the growth potential of these businesses that over time they will justify what today looks like high valuations.

He adds that the companies in sectors that do not look especially attractive for the years ahead are actually already lowly valued.

Premier Miton's James says European companies' leading role in addressing climate-related issues will be a major driver of investment returns in the years to come.

He says: "Roll on 10 years and the picture appears to be very different. Europe is leading the way globally, tackling climate change with European companies at the vanguard. Any self-respecting investor searching for companies that are committed to playing their role in making the world more sustainable should look no further than Europe."

Chris Elliott, who jointly runs the Evenlode Global Equity fund, says he presently has 37 per cent of the fund’s capital deployed in European equities.

He says: “We continue to see good opportunities for investment in Europe.

“However, we stress that the prospects for growth are uneven, and that careful stock-picking is required. We think three key factors make a company attractive: structural market growth; a durable competitive advantage; and supportive investment.

“When all three are present, companies are often able to grow cash flows ahead of market expectations, regardless of their listing geography.”

Part of the reason investors identify a particular political risk in the Eurozone dates back to 2011, when the European Central Bank lifted interest rates in anticipation that economic growth was strong and inflation was imminent.

The rate rise precipitated a sovereign debt crisis as the market feared the impact of higher borrowing costs, and a crisis and further recession occurred.

This month, the ECB faced a similar scenario with inflation rising and growth returning and announced what the market viewed as a very limited 'tapering' of its asset purchase programme, and was sanguine.

The more moderate measure than the blunt instrument of an interest rate rise being viewed as less likely to cause significant economic or stock market harm.

Hugo Le Damany, economist at Axa Investment Managers, notes the announcement from the central bank left the bond market “nonplussed”, and if there were concerns, as in 2011, that the pace of monetary tightening was too fast, then it is in the bond market where this reaction would mostly have been felt, with yields rising.

The ECB also upgraded its GDP forecast for this year to 5 per cent from the previous estimate of 4.6 per cent, while continuing to expect inflation to be below its 2 per cent target rate over the medium term.

Paillat says the Eurozone’s response to the pandemic, which, in addition to interest rate cuts and monetary policy initiatives also included increased government spending, means the bloc may escape from the “secular stagnation” trend that has hindered equity markets over the past decade.

This would, he says, potentially change the long-term outlook for European equities, even if the shorter-term outlook is uncertain due to concerns about emerging markets and the pandemic.

Elga Bartsch, head of macro research at the BlackRock Investment Institute, says: “We recently upgraded European equities to overweight, based on the broadening recovery with the vaccination rollout accelerating. Valuations remain attractive relative to historical levels, and thanks to strong earnings these look even more attractive than at the start of the year.”

Stefan Gries, who runs the BlackRock Greater Europe investment trust, says the key to the extra spending undertaken as part of the pandemic recovery plan is that it will likely boost areas of the economy, such as sustainable technology, in which it had not previously been feasible to invest.

He says this creates new opportunities for investors, away from the quality but expensive companies and the cheap but challenged cyclical businesses.

He expects the impact of the extra spending to be felt in the market from late 2022.

Niall Gallagher, investment director for European equities at GAM, says European equities are one of the few markets where valuations do not look overly stretched. He says because of delays with its vaccine programme, the Eurozone economy is a little behind much of the rest of the world in terms of economic growth, which he notes is a positive as there is more growth still to come from the Eurozone than the rest of the world.

He says this growth trajectory “broadens” the range of stocks in which he wants to own in Europe. He says the traditional type of equities he wanted to own in Europe included tech companies and luxury goods companies, both of which he still believes in, in addition to the companies that benefit from a growing economy.

Gallagher says: “Continental Europe was a little later in getting Covid vaccination programs operating at full speed than some other regions. That aspect of rebounding economic growth is yet to come, notably with regard to travel. Some European businesses were turbo-charged by the impact of Covid (for example, both Finecobank and Zalando benefiting from the shift from offline to online business, and Adyen from the accelerating shift to cashless).

“As a result, we have seen very strong earnings growth in our portfolio, with accompanying positive forward guidance.

At the same time, European valuations are un-stretched relative to other asset classes or regions, and we believe this bodes well for the sector."